| Online: | |

| Visits: | |

| Stories: |

The SEC’s just been caught colluding with the banks it’s supposed to regulate

Reuters finance blogger Felix Salmon had a post earlier this week headlined “Yes, the SEC was colluding with banks on CDO prosecutions.” This ought to be huge news. The Securities and Exchange Commission is one of the main agencies that’s supposed to be regulating Wall Street. But they’ve been essentially caught red handed working together with Goldman Sachs to make it looklike Goldman was paying a huge fine when really they’re paying a small one. Sadly, though, the story probably won’t get much attention from the general public because the CDO prosecution issue is a little obscure and it hasn’t really been in the news for years.

But people ought to understand this story. It’s a very big deal not so much because the case was all that important, but because it speaks directly to the question of whether or not our government institutions have the will and ability to regulate the financial sector.

What’s a CDO?

To understand what that means, start with something simple like a mortgage or an auto loan. The good news for a lender is that he earns a profit — the interest rate — on the money leant out. The bad news is that the borrower may default.

So now imagine you had ten roughly similar loans. A person who owned-one tenth of each of those loans would earn the same interest rate as someone who owned a single loan, but the odds of all ten loans defaulting simultaneously are low. A package that consisted of one-tenth of ten separate loans would be a very simple form of collateralized debt obligation.

The same principle can be applied, however, to create very complicated securities. Investment banks did a lot of this during the pre-crisis years, and belief that these securities were very safe fueled a lot of lending activity. What did banks do wrong?

What did banks do wrong?

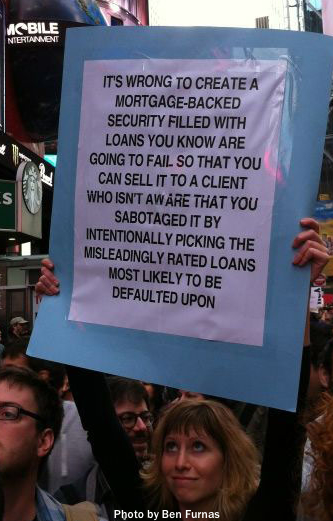

One set of allegations involved banks creating and marketing CDOs that they believed to be risky, marketing them as safe, and then making side-bets that the CDO in question would go bust.

Another set of allegations involved banks marketing CDOs whose contents were actually selected by third parties — third parties who were making bets that the CDO would go bust.

In either case, the basic claim was of fraudulent marketing of the security. In general, people who sell products that fail are held in low regard. People who sell products that they know to be likely to fail are held in lower regard. People who sell products that they in fact intend to fail and who’ve arranged financial bets such that failure will result in higher profits are held in even lower regard.

Once the full extent of the financial crisis became clear, these sort of deals were widely criticized and the Securities and Exchange Commission (SEC) which is supposed to prevent misconduct in financial markets began a series of investigations.the SEC’s conclusion was extremely fishy

What happened?

What’s wrong with that?

What do we know now?The banks paid not to settle one CDO suit, but to settle all the CDO suits

How do we know?

Here’s the nut, per Beck. Robert Khuzami is the top enforcement guy at the SEC. David Kotz is the SEC’s inspector general, charged with oversight of the agency’s performance:The SEC filed its case against Goldman and Tourre on April 16, 2010. Three days later Goldman reached out with a $500 million settlement offer, according to an email that Reisner sent Khuzami. Although that proposal was close to the final payment, it took another three months to announce a settlement. As Khuzami described to Kotz, Goldman wanted a global settlement that resolved not just the Abacus investigation but the SEC’s probes into roughly a dozen other Goldman CDOs.

Khuzami didn’t want to give Goldman that public victory. When the SEC and Goldman announced on July 16, 2010, that the investment bank would settle the Abacus case for $550 million, the SEC said in a press release that the settlement “does not settle any other past, current or future SEC investigations against the firm.”

Khuzami was determined that Goldman’s payment only be linked to ABACUS. “This was not a $550 million settlement for 11 cases,” Khuzami told Kotz. “We may tell Goldman that we are concluding our investigations in these other matters without recommending charges, but that doesn’t mean we’re settling them. And that was an important point for us, because we didn’t want them out there saying, you know, they settled 12 CDO investigations for an average of $30 million each, and, you know, didn’t [Goldman] get a great deal.”

In other words, Khuzami agreed to a global settlement with Goldman, but then lied about what he’d agreed to. And he more or less got Goldman to go along with the lie as part of the agreement. There is still no smoking gun to prove that the exact same process played out in the settlements with the other banks, but the pattern of one-and-only-one prosecution followed by a settlement is the same everywhere. It’s always been a suspicious pattern. And now in the one case we’ve been able to look into, we know there was collusion. It’s deeply suspicious.

How important is this CDO thing? Did this cause the crisis?

So is this story important?

Where is Robert Khuzami now?

What is the unemployment rate?

The unemployment rate is the number of number of people looking for a job divided by the total size of the labor force. This means that the unemployment rate often misses a lot of discouraged people who have stopped looking for work but would love a job if they could find one.

The flipside of the unemployment rate is the employment rate, the ratio of people with jobs to the total size of the labor force. It is rare to hear anything about the employment rate. Instead, a more commonly discussed statistic is the employment-population ratio-the ratio of people with jobs to all people, including children, retirees, homemakers and others who aren’t in the labor force.

The unemployment rate rose sharply in the wake of the 2008 financial crisis, and has been falling since 2010. Currently it stands at 6.7 percent which is still high by historical standards.

Source: http://nesaranews.blogspot.com/2014/04/the-secs-just-been-caught-colluding.html