Financialization’s Self-Destruct Sequence

August 16, 2012

We are in the latter stages of financialization’s self-destruct sequence.

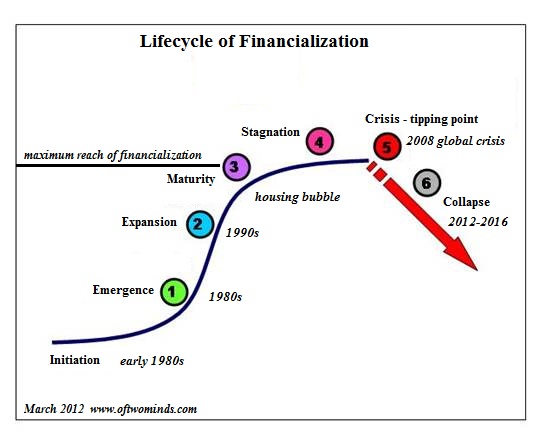

Like all systems that follow an S-curve of growth and decay, financialization cannot return to its growth phase. I addressed the impossibility of reflating asset and credit bubbles in Let’s Pretend Financialization Hasn’t Killed the Economy (March 8, 2012).

But there is another dynamic at play: a self-destruct sequence triggered by central bank and Central State efforts to reflate asset and credit/leverage bubbles. All central bank and State policies aimed at driving capital into risk assets boil down to reflating phantom assets purchased with debt by issuing more debt that is based on newly issued phantom assets.

Phantom assets purchased with debt cannot be reflated by issuing more debt that is based on newly issued phantom assets. Piling more debt/leverage on a sandpile of phantom assets (CDS, bonds that cannot possibly be paid back, empty condos in the middle of nowhere, etc.) only heightens the probability that the unstable pile will collapse.

The implicit Central Planning campaign to trigger “mild” inflation is part of the self-destruct sequence. Central planners metaphorically fight the last war, or at best the last two wars, and so they remain blind to any dynamics that did not exist in their case studies.

In the 1970s, central bank easing and Central State stimulus sparked a nasty bout of accelerating inflation. This reduced the weight of debt because wages inflated along with goods and services.

Now that labor is in surplus globally, wages are not keeping pace with inflation. This completely changes the dynamic of “mild” (3%) inflation: as the purchasing power of earned income declines, servicing debt becomes more burdensome. Inflation only renders debt less burdensome if wages rise at the same rate as the cost of goods and services.

In a decade of “mild” inflation and stagnant wages, households will experience a very real-world 30+% decline in their income. Meanwhile, their debt payments remain unchanged.

“Mild” inflation in an era of stagnant earned income will crush households, forcing liquidation or renunciation of debt. What happens as debt service costs rise as a percentage of real net income? There is less cash for consumption, and so the consumer-dependent economy spirals down. Credit is poured into the banking sector, but little trickles down to high-debt, stagnant-income households. This is deleveraging writ large.

What happens when central bank financial repression–lowering the yield on cash to near-zero–causes pension plans to fail and savings to earn negative real returns? Households must save more income to compensate for the destruction of yield by Central Planners.

These mutually reinforcing dynamics feed the self-destruct sequence’s inevitability. Add up the self-destructive forces……..