| Story Views | |

| Now: | |

| Last Hour: | |

| Last 24 Hours: | |

| Total: | |

Spring 2016 Newsletter

The markets have rallied back up, and once against have fairly rich valuations. But there is considerable uncertainty in the market, and some high quality companies are trading at lower prices than they were a few months ago.

Here’s a list of three companies that I believe are reasonably valued, and that may become even more attractive if another market decline were to occur.

Magellan Midstream Partners LP (MMP)

I briefly mentioned Magellan in my December newsletter, and I certainly believe it deserves a more direct focus here. It’s a fairly conservative pick in the troubled pipeline industry, offering a decent yield and strong distribution growth. It’s my current preferred selection in the industry.

Unlike many other pipeline operators, Magellan primarily focuses on transporting refined products, and they’re the largest refined products pipeline company in the country. They have 9,500 miles of refined pipelines, 50+ terminals, and 40+ mm barrels of storage facilities, and access to about 50% of the country’s supply. To round that out, they also have 1,600 miles of crude products pipelines and 20+ mm barrels of crude storage facilities. Lastly, they have 5 marine storage facilities.

Their focus on refined products is what has largely protected them from the oil price crash. Their unit price has taken a big hit due to a reasonable valuation correction, but their actual operating numbers remain strong, and the distribribution remains very safe. This is because most of their volume is demand-based rather than supply-based. As long as U.S. consumers and businesses keep using large amounts of gasoline, diesel fuel, jet fuel, petrochemicals, lubricants, asphalt, and oil-based plastics, then Magellan should continue to do very well.

The company currently pays a distribution yield of about 4.5%, with double-digit distribution growth over the last decade and a half. The distribution growth from 2014-2015, straight through this crash of oil prices, was just over 15% for the year. MMP management expect 10% distribution growth in 2016 and at least 8% distribution growth in 2017.

They currently have over 1.3x distribution coverage, meaning they have over 30% more cash flow than they pay in distributions, which is much higher than most other MLPs. Magellan aims to keep this number above 1.1, so they’re far above their target and playing it safe. They also have a lower than average debt/EBITDA ratio of under 3, and one of the industries highest credit ratings at BBB+.

The partnership does face some headwinds from low commodity prices that affect about 15% of their business, and reductions in supply from some basins as well as the potential for defaults from some of their troubled customers that can affect Magellan’s performance to a degree.

A long term risk to Magellan is a reduction in the use of oil products. An example would be Tesla’s upcoming Model 3, or Chevrolet’s upcoming Bolt, which both aim to be roughly $30k all-electric vehicles with 200+ mile battery ranges between charges. The electric car industry is fragile, with little market penetration, reliances on federal subsidies, and a lack of charging infrastructure. But as lower priced electric vehicles with ranges that can comfortably fit any normal commute become commonplace, this could change. Overall though, industry estimates for the market growth of these kinds of vehicles aren’t large enough to materially affect Magellan through 2020 at least.

One of the strongest points in Magellan’s favor is the fact that they have no incentive distribution rights (IDRs) to pay. Many MLPs have to pay up to 50% of their cash flow to their general partners, but Magellan is 100% owned by the public. So, Magellan has all of the tax advantages of being an MLP, but doesn’t have to deal with the downside of IDRs. This effectively means they have a lower cost of capital than most of their peers. When IDRs cap out at 25% or so, like Brookfield Infrastructure Partners, then they’re not much of a drag on growth. But when IDR caps are as high as 50%, like many MLPs are, it can limit the types of investments that an MLP can profitably make while still increasing its per-unit distributions. Magellan is free of this problem entirely.

They also don’t currently rely on raising capital with equity. Many MLPs ran into trouble in 2015 when they relied on selling units to raise cash, but their unit prices were cut in half or worse, leading to that suddenly being a poor way to raise money. Magellan has the option to raise equity capital if a huge opportunity comes along, but they don’t need it for general growth and operating expenses, and haven’t increased their number of outstanding units in the last 5 years. They keep the distribution coverage high enough that they pay a growing distribution while using excess cash to internally fund investments for growth, and rely on conservative levels of debt financing.

Wrapping It Up Into a Valuation

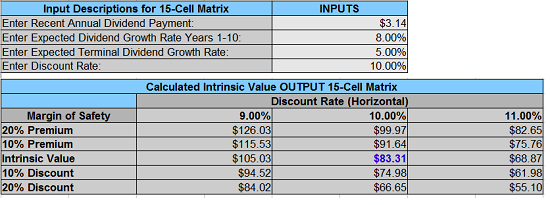

Magellan’s most recent quarterly distribution was $0.785/unit, which is $3.14/unit annualized. This is a distribution yield of about 4.5%. Since inception, their distribution growth rate has averaged about 13% per year.

The performance, therefore, has been oustanding. A 4-5% distribution yield with a 10-15% distribution growth rate over a decade or more translates into market-crushing performance. So for the forward period, I’m not going to use those numbers. Instead, I’ll use more conservative estimates that assume Magellan must slow down, must face more headwinds, must deal with a more saturated pipeline industry, must face the rise of electric vehicles, and so forth.

Here’s a dividend discount model analysis of MMP, using 8% distribution growth for the next decade and 5% thereafter, and a 10% target rate of annualized return:

Source: Dividend Monk Toolkit Excel Calculation Spreadsheet

The result is a valuation estimate of $83. In comparison, Morningstar currently has a fair value estimtae of $76, and Argus Research has a price target of $85.

The current price in the low $70’s places it about 15% below my fair value estimate, implying that expected returns going forward should be over 10%/year with a margin of safety. It’s not a very high hurdle to step over, and therefore I believe that Magellan is a great risk-adjusted opportunity.

If you want an even larger margin of safety than the current price offers, Magellan units have very attractive option premiums. You can sell a July 16, 2016 cash-secured put with a strike price of $65 for about three dollars. This means that during the next four months, if Magellan stock goes below $65, you may have to purchase it for $65, which counting the premium would give you a cost basis of about $62. Then, you’d have a great cost basis to hold it for the long-term. Or, if Magellan remains above $65, you would keep your three dollars per unit, which translates into a return of about 4.8% for just a four month period, and you could write another option at that point, and continue this strategy until you own it.

CSX Corporation (CSX)

I believe it’s time to buy the railroads, and it’s really a toss-up between CSX and UNP at this point, in my opinion. They’re the two largest remaining pure-play Class I railroads in the United States, and UNP operates in the western two-thirds of the country while CSX operates in the eastern third of the country.

UNP is, by many metrics, the slightly better company. Their long stretches of track along the lesser-populated region of the country are good alternatives to trucks, and they have access to Mexico for the transport of cars. But this comes with an earnings multiple that is about 2 higher than CSX, and a slightly lower dividend yield.

Mike recently published articles on both of them, and I think both are strong investments. An investor would likely do fine diversifying into both of them, if they want railroad holdings for the entire continental United States. For this article, I’ll focus on CSX.

Downtrodden

The global crash in commodity prices has hurt the U.S. railroads. Coal in particular is down, both as a source of energy and as an ingredient in steel. Low natural gas prices have all but made coal obsolete as an energy source for new energy plants, especially considering that it’s one of the dirtier sources anyway. Export coal volumes are hurt by the strong U.S. dollar and a weak Chinese economy. Metallurgical coal used in steelmaking is down as well, also due to Chinese weakness and other global issues.

Many other goods in the economy have declining volume, and the massive reduction in diesel prices has made trucking more affordable, which can eat into railroads market share. As such, CSX has seen its stock price drop from about $37 to now around $25.

Despite the big stock price hit, the company is doing fine. Although revenue was down 13% for 2015 compared to the year prior, 2015 EPS was higher than 2014. Going into 2016, the company expects mild EPS declines compared to 2015, as continued volume weakness, especially from coal, is offset by reducing the number of engines and workers. Thanks to the the advances in automation technolgies over the last two decades, the railroads now have highly flexible business models that allow them to shrink and expand to meet cyclical demand, which is good for just about everyone except of course the rail workers. All in all, CSX deserved a price correction, but losing a third of the stock price puts it into oversold territory, in my opinion.

Analysists expect EPS in 2016 to be $1.86 compared to $2.00 in 2015. But with current information, they expect CSX’s 2017 EPS to be back up to over its 2015 figure. We’ll see what happens, but the point is, CSX adusts to changes in volume.

An Opportunity

A project is expected to be completed this year that will double the capacity of the Panama Canal, and increase the maximum size of ships that can pass through. This is expected to increase shipping volume between Asia and the east coast of the United States.

Currently, materials and products that ship between the eastern half of the United States and Asia are usually shipped between Asia and the west coast and then railed between the west coast and the eastern half. But with direct access to ports along the east coast with larger container ships thanks to the panama canal expansion, the two western U.S. railroads are expected by some analysists to lose market share to the two eastern U.S. railroads. Ports along the east coast are expanding to allow for these larger ships, in expectation of this increase. Some estimates are that the intermodal market share for CSX could increase from 20% to 25% over the next five years. When comparing CSX to UNP, that’s a factor to consider, especially with CSX consistently being at the lower valuation.

Both remain strong picks, in my view.

Dividend Growth

Estimating the actual volume growth or shrinkage of railroads over a long period of time is nearly impossible, due to how cyclical it all is. The good news is that unlike many other industries, you don’t need very accurate estimates; you just need to know how management intends to allocate their capital, assuming no fundamental changes radically reduce rail volume.

Revenue for CSX in 2016 is not much higher than it was in 2008, for example, and yet EPS has almost doubled during those eight years. Shareholder returns from railroads come mostly from dividends and sharebuybacks; not from core growth.

If over the next ten-year period, CSX has 0% net volume growth and 2% annual pricing growth in line with inflation, then revenue growth will average 2% per year. The dividend yield is about 2.8%, and the company historically buys back stock and reduces its share count by about 2-4% per year, which makes sense given that they have an earnings yield of about 7%, which mostly goes to dividends and buybacks.

Adding this together, if the dividend payout and debt/equity ratios stay relatively static, you can reasonably expect a 2.8% dividend yield and a forward dividend growth rate of about 4-6%, based on 2% annual price increases and 2-4% buybacks. That comes out to a total rate of return of about 6.8%-8.8% per year, with zero volume growth, from a boring railroad investment. Any volume growth would be in addition to that.

Rockwell Automation (ROK)

This is a good candidate to buy on dips. The company has excellent long-term growth prospects but the valuation is at the high end of what’s fair, with a current P/E ratio of about 18.

Rockwell is a provider of industrial automation products and services. This includes selling automation hardware and software to companies, and also includes experts that can implement those products for a company. Their products can cover both discrete and process solutions, and they have useful lifecycles of over ten years in most cases. Their software and hardware are unique, with high switching costs. Customers tend to be quite “sticky”, and therefore Rockwell has a durable competitive advantage.

I run the electrical engineering department of a small organization that I work for, and we’ve been using the same automation products from one of Rockwell’s competitors since I took the job, despite changing most other things over time. My predecessor used them, and I still use them, simply because they work well enough and the software engineers would have to change a lot of code to start working with a new system. I continue to buy tens of thousands of dollars of those systems, even as they increase the price regularly, because price isn’t our only decision point. I’ve examined other systems, and have never found a compelling reason to switch to a different one. In short, software switching costs can be high due to the need for re-integration and additional software writing and testing, and it creates a moat and pricing power.

Although Rockwell is in a low-growth period due to global economic issues, they’re a leader in an industry that has nowhere to go but up. Rockwell estimates that the global potential market for their products increased from $65 billion in 2010 to $90 billion in 2015.

Strong Cash Flow

Rockwell has had fairly unimpressive revenue growth over the last ten years, but they’ve enjoyed strong EPS growth, book value growth, and dividend growth. Their balance sheet is safe but not spectacular. What really shines is their free cash flow; they’re one of the uncommon companies that consistently generate more in free cash flow than they report as earnings. So, while the price to earnings ratio is currently 18, the price to free cash flow ratio is under 15. Suddenly the company looks a lot more attractively priced.

The company doesn’t waste it, either. Over the last five years, the company has increased its dividend by over 15% per year on average, while consistently reducing their outstanding share count. The current dividend yield is about 2.7%. Forward dividend growth should slow down as we enter a more difficult period for global growth, but Rockwell remains in a position to produce consistent dividend growth.

Wait For It…

Rockwell was at its high in 2014, at over $125/share at one point. In January of 2016, during the market correction, Rockwell stock traded nearly as low as $90/share. Now, it’s back up to $107. The market has been bipolar about it, constantly changing market price due to variances in global growth expectations.

Buying at $107 would be a solid purchase, in my opinion. But the stock is also a good candidate for selling puts, based on the price of the premiums, the stability of the company, and the volatility of the stock.

You can sell a July 2016 put for a strike price of $100 and earn a $4 premium. If the stock declines to under $100 in the next four months, then you’d buy it for a cost basis of $96, which is only 13x current FCF. If the company remained over $100 by expiration in mid July, you’d keep the premium anyway, and enjoy a return of over 4% in a period of a little over four months, and write another option. You can get paid like this to eventually buy at a very attractive cost basis.

Conclusion

Although overall market valuation remains fairly high at the moment, there are plenty of opportunities to establish long-term positions in cyclical industries. Railroads, best-of-breed pipelines, and industrials are all facing troubles at the moment, but their long-term potential remains optimistic and their valuations remain reasonable.

Source: