| Story Views | |

| Now: | |

| Last Hour: | |

| Last 24 Hours: | |

| Total: | |

SIF Portfolio: Tough choices in the face of macro uncertainty

As I write on Tuesday, the market is full of unanswered questions. Article 50 and Brexit are looming. We’re waiting to find out whether the US Federal Reserve will increase interest rates in March. If it does, will the Bank of England follow suit later this year, now that inflation is rising?

The outlook for oil and energy prices is also uncertain. The price of crude oil has fallen by 10% over the last week. Fears that US shale producers will flood the market and cancel out OPEC production cuts have led to a widespread selloff. On the other hand, it’s also possible to argue that this pullback is just a routine period of consolidation in the longer-term recovery of the oil market.

Whatever happens, changing energy prices, interest rates and inflation will affect many of the stocks we invest in. So should I be tweaking the Stock in Focus screen to search for companies that might benefit from higher interest rates or cheap oil? I don’t think so.

Predicting the future is just too difficult. There are so many variables involved that I’m almost certain to guess wrongly. If hedge funds with supercomputers, teams of PhDs and huge archives of data can’t get it right, what chance have I got?

More importantly, the SIF portfolio is driven by stock-specific fundamentals and quantitative factors. This bottom-up approach is at odds with the top-down approach I’d have to use if I wanted to direct my exposure to specific sectors of the market.

How I handle macro risks

I won’t be making any changes to my investing policy for the SIF portfolio in the light of macro developments, including Brexit. I’m confident that if the economic environment changes, I’ll be able to rely on the fundamental criteria in my screen to highlight potentially attractive stocks.

Of course, this doesn’t mean that I don’t pay any attention to macro risks. My defence against the unknowable is to try and maintain a reasonably diversified portfolio. Sometimes, this means rejecting stocks I might otherwise buy.

One example of this is City of London Investment Group. This high-yielding small-cap fund manager has qualified for my screen this week. Unfortunately I already own a small-cap fund manager in the form of Miton Group, so CLIG isn’t an option.

A defensive opportunity?

One of the biggest and most persistent problems I’ve faced in building the SIF portfolio has been the lack of eligible defensive stocks. My original target was for the portfolio to maintain an approximate balance between cyclical and defensive stocks. It’s safe to say that so far I’ve failed. As things stand, just three out of the 15 stocks in the portfolio are defensive. And one of those is Russian.

However, back in February I introduced a relaxed version of my screen inspired by the work of Jim Slater. This is intended for use when my full-strength screen dries up for extended periods of time. My goal was to prevent the SIF Portfolio sitting in cash during bull markets, missing potential gains.

Privately, I was also hoping that the relaxed screen would provide me with a more ready supply of defensive stocks for the portfolio. So far, that’s not really happened. As you can see from the screenshot below, the relaxed screen results are still almost 100% cyclical.

SIF screen results on left, relaxed screen results on the right:

Almost, but not quite.

Right at the bottom of the list is motor insurance group Hastings. According to the Capita Dividend Monitor report, non-life insurance firms are defensive, not cyclical.

Good and improving

My original plan was to only use the relaxed screen after four consecutive weeks of non-performance by the main screen.

However, such is my need for defensive stocks that I’m going to stretch the rules and consider adding Hastings to the portfolio this week. The portfolio doesn’t currently contain any insurers and is woefully short of defensive stocks.

Hastings has also impressed me recently. Unlike peers such as Direct Line and Admiral, Hastings share price was not hit by the Lord Chancellor’s decision to set the Ogden rate to -0.75%. One reason for this may be that Hastings remained profitable at an underwriting level even after booking a £20m one-off hit from Ogden. Its combined ratio for 2016 was 91.3%, better than most comparable peers.

The company’s 2016 results were generally quite good. Gross written premiums rose by 25% to £769.0m, while operating profit climbed 21% to £152.1m, pre-Ogden. Net debt fell from 2.1x to 1.9x EBITDA despite the Ogden hit. Further progress in all areas is expected this year.

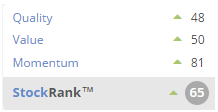

Stockopedia’s computers shared my positive view of these figures. Hastings’ StockRank has risen 19 places to 65 over the last 30 days. This increase has been driven by improvements in all three rankings:

Should I add Hastings to the SIF portfolio?

Growth trumps value

A ValueRank of 50 isn’t great. But this is a growth and income stock, not a value play. Hastings’ rapid earnings growth means the market is looking forward.

The group’s trailing P/E of 20 won’t provide much downside protection if things go wrong. But I’m comforted by the earnings yield (EBIT/EV) of 6%. This suggests to me that the shares are actually quite reasonably valued. If profits continue rising and leverage continues to fall, then shareholders should benefit from this value.

Another point worth considering is that Hastings has a GrowthRank of 99. This metric isn’t used in the StockRank calculation, but it is available for all stocks. I think the figures speak for themselves:

Deceptively good quality

Deceptively good quality

A QualityRank of 48 seems worrying, but Hastings scores well on most of the metrics for which it qualifies as a financial stock:

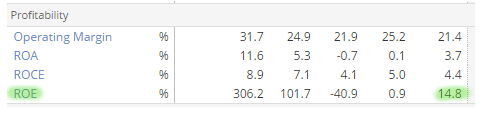

I’m reassured by the high Piotroski F-Score of 7, which suggests the firm has no serious financial issues. The net margin of 10% is also decent, but the long-term average return on capital employed (ROCE) of 5% seems less so.

However, I’m not sure that ROCE is the best measure of profitability for insurers. I think that as with banks, return on equity is more appropriate. Here, Hastings scores reasonably well, with a trailing RoE of 14% according to Stockopedia:

It’s all about momentum

It’s all about momentum

We’re in a bull market and Hastings is a growth stock. No surprise then that the firm’s main StockRank strength comes from its MomentumRank of 81:

There’s really nothing to pick fault with here, in my view. Broker forecasts for 2017 were significantly upgraded after last year’s interim results and have remained steady since. These figures put the stock on a forecast P/E of 12 with a prospective yield of 4.6%.

In my view, this could be an attractive entry point for the stock. I am going to press on and add Hastings to the SIF Portfolio this week.

As always, I’d really appreciate your feedback. Please let me know what you think in the comments below.

Source: http://www.stockopedia.com/content/sif-portfolio-tough-choices-in-the-face-of-macro-uncertainty-175671/