| Story Views | |

| Now: | |

| Last Hour: | |

| Last 24 Hours: | |

| Total: | |

SIF Portfolio: Why Coats Group could beat the market in 2017

For Stockopedia junkies like me, one of the interesting aspects of corporate results season is seeing how each company’s results affect its StockRank. The effects of a fresh set of figures can be dramatic.

By ignoring whether a stock is cyclical or defensive, the StockRank system often highlights value in areas where market sentiment and broker forecasts suggest that stocks might be fully valued. Housebuilders are one example, mining stocks and big retailers are two other which currently score highly for value.

I recently added FTSE 250 miner South32 and housebuilder Redrow to the SIF Portfolio after these firms’ interim results boosted their StockRank metrics. These same figures also caused them to qualify for the Stock in Focus screen.

However, although my screen results are sorted by StockRank, stocks qualify for the screen based on my own set of fundamental criteria. StockRanks are not used for stock selection and companies which qualify may not have rising StockRanks.

One example is today’s stock, thread manufacturing company Coats Group. This 250-year old group has recently qualified for my screen.

Coats reported full-year sales of $1.5bn last year. It’s the global market leader in industrial thread for the clothing and footwear industry. Customers include Adidas, Burberry and Next. The group is also a big player in the US craft market and makes various other types of industrial yarn.

When Graham Neary reviewed the firm’s 2016 results on 24 February, Coats had a StockRank of 97. Now that last year’s accounts have been added to the Stockopedia database, Coat’s StockRank has fallen 20 places to 77. That’s still a decent score, but isn’t outstanding.

However, I am attracted to Coats’ market-leading business, which would add useful retail exposure to the SIF portfolio. Sentiment towards the company has also improved markedly since December, when Coats agreed a deal with the UK Pensions Regulator to resolve its pension deficit. This has enabled Coats to restart dividend payments. I believe it should also drive strong growth in free cash flow from 2018.

Although Coats’ share price has doubled over the last six months, I think there’s a good chance of further gains. I believe this stock is definitely worth considering for the SIF portfolio.

Value: serious potential

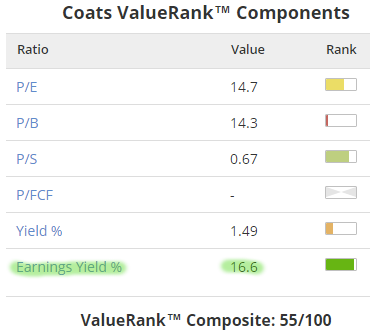

Coats’ ValueRank of 55 isn’t obviously attractive. But in my view, a closer look indicates the potential for attractive shareholder returns.

Regular readers will know of my affection for Earnings Yield (operating profit / enterprise value). Coats’ earnings yield of 16.6% is pretty good. To put this in context, the threshold needed to qualify for the Stock in Focus screen is 8%.

The reason I like earnings yield so much is that it combines valuation with profitability. A high earnings yield backed by strong free cash flow arguably makes metrics such as the P/E and operating margin irrelevant.

One weakness in this case is that Coats’ earnings yield isn’t backed by free cash flow. Nor is it reflected in the group’s low dividend yield. So what’s going on?

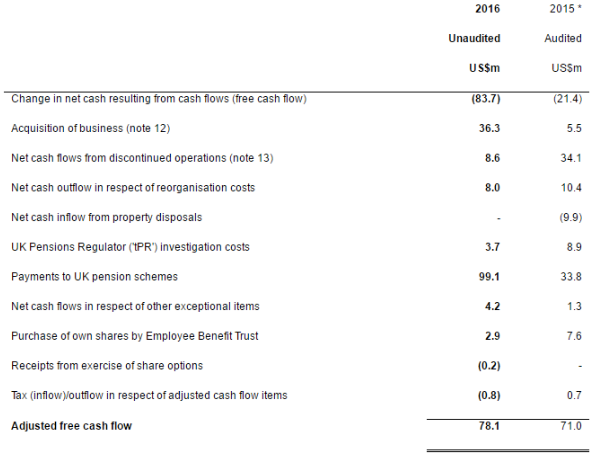

Free cash flow: Although Coats reported adjusted free cash flow of £78.1m last year, the group’s actual free cash flow was -£83.7m.

The biggest single adjustment was a £99.1m contribution to the group’s UK pension schemes, which have a collective deficit of $627m. Under the terms of its recent agreement with the pension regulator, Coats will have to make an upfront payment of £255m to these schemes this year, after which annual contributions will fall to £15m.

So in exchange for some short-term pain, free cash flow from 2018 onwards should be dramatically improved.

Obviously this rosy picture rests on the assumption that the remaining pension deficit will eventually fall as interest rates and bond yields improve. There’s a material risk that this won’t happen, but it’s one I’d be prepared to take to invest in an attractive business.

Dividend yield: Coats reinstated dividend payments last year, after suspending them in 2011. The outlook is for 20% annual dividend growth over the next two years. I’d imagine that from 2018 onwards, Coats payout capacity should improve significantly. So I don’t see the low trailing yield as a concern.

Book value: Coats currently trades at a whopping 14 times its book value. But if you ignore the firm’s various pension deficits, Coats has a P/B of about 1. As with other elements of the group’s valuation, this could be attractive if you believe interest rates will rise in the-not-too-distant future, reducing such deficits.

Strong underlying quality

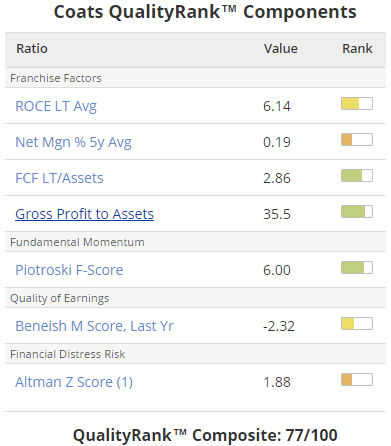

Coats’ QualityRank of 77 suggests a more attractive picture. And it is:

The stock’s five-year average return on capital employed of 6.1% isn’t outstanding. But ROCE appears to be improving. The group’s adjusted measure rose from 33% to 39% last year. Stockopedia’s more inclusive and standardised measure of ROCE rose from 8.5% to 16.4%, while operating margin rose from 7.6% to 10.5%.

An average free cash flow to assets ratio of 2.9 also shows promise. So too does the gross profit to assets ratio of 35. These ratios suggest to me that the group has decent manufacturing profit margins and an underlying ability to generate free cash flow. My thesis is that if the group can put its historic pension problems to bed, these characteristics should lead to attractive returns for shareholders.

I’m also reassured by Coats’ Piotroski F-Score of 6. This suggests that both the operating business and the parent company’s balance sheet are in decent health. Overall, I’ve no serious concerns here.

City upgrades could drive further gains

Coats’ share price has risen by 95% to about 57p over the last six months. Most of this dramatic increase happened in December, when the pension settlement was announced. Coats had been under investigation by the pension regulator since 2013, when Coats was known as Guinness Peat Group.

Before the settlement, Coats Group could probably have been described as a special situation investment. There were specific risks that were hard to measure. Although the big gain since December could make it seem as though new buyers have missed the boat, I don’t think that’s true.

I’d argue that the current valuation is probably a reasonable valuation of the group’s underlying business. Further growth seems entirely possible, although as is noted in the recent results, the short-term outlook carries some uncertainty:

Brokers expect adjusted earnings to rise by 18% to 5.8 cents per share this year. At about 57p, the stock trades on a 2017 forecast P/E of 12, with a prospective yield of 2%.

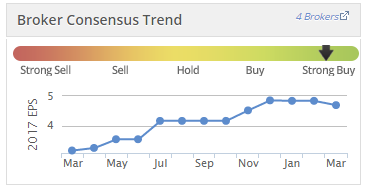

Consensus forecasts for 2017 were upgraded repeatedly last year, which suggests earnings momentum is strong and that further upgrades may be possible:

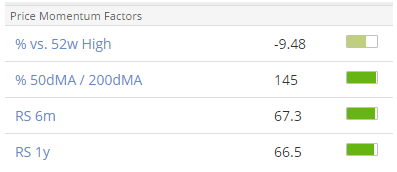

Price momentum is also strong, as the share price is within 10% of its 52-week high and showing very positive technical indicators:

In my opinion, Coats Group’s market-leading scale, undemanding valuation and improving balance sheet may well deliver attractive shareholder returns for shareholders. So I’m going to add a slice of the stock to the SIF Portfolio this week.

Disclosure: Roland owns shares of Next.

Source: http://www.stockopedia.com/content/sif-portfolio-why-coats-group-could-beat-the-market-in-2017-177008/