| Story Views | |

| Now: | |

| Last Hour: | |

| Last 24 Hours: | |

| Total: | |

SIF Portfolio: Can I clean up with McBride?

How many own-branded goods end up in your shopping trolley each week? I’m guessing there are a fair number.

If so, there’s a good chance that some of them are produced by this week’s SIF Portfolio candidate, McBride.

This FTSE Smallcap listed stock produces private label household and personal care products. Judging from the pictures on the company’s website, the group’s customers include Sainsbury’s and Morrisons, plus others. McBride also has a few of its own brands, such as Oven Pride, but private label manufacturing is the firm’s main business.

After a troubled few years leading up to 2015, management launched a transformation plan with the slogan Repair, Prepare, Grow. This aimed to improve the profitability and quality of the firm’s manufacturing operations, before targeting fresh growth.

Progress so far has been encouraging. McBride’s return on capital employed rose from 5.4% to 16.5% in 2016 and cash flow has improved significantly. The group’s recent interim results showed a further improvement in profitability, with the company’s measure of return on capital employed rising from 23.6% to 28%.

To me, these figures suggest the firm’s transformation programme is working. The firm’s 2015 target was to reach an ROCE of 25-30% in three-five years. To put this target in context, the equivalent figure at the end of June 2014 was 12.7%.

McBride’s StockRank has risen from 83 to 93 over the last year and the firm has recently qualified for my Stock in Focus screen. The SIF Portfolio’s chronic need for defensive stocks means that McBride is a serious candidate for a buy, unless I find something nasty in the figures.

The right value

Paul Scott commented on McBride’s interim results on 22 February, noting that “that valuation looks about right to me”. The stock has risen by more than 10% since then, so am I too late to join the party?

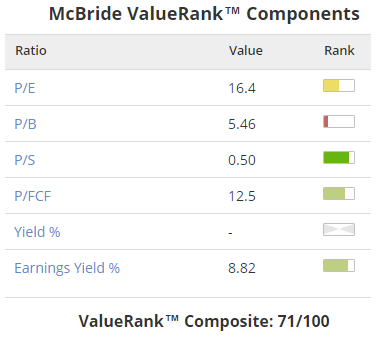

Stockopedia’s ValueRank uses trailing twelve month (TTM) figures. Based on these figures I’d be tempted to agree with Paul’s view:

A P/E of 16.4 seems reasonable but not cheap. The yield isn’t shown here, possibly because McBride has returned cash to shareholders through a B-share scheme rather than a dividend over the last year.

Shareholders have actually received 3.8p per share over the last twelve months, giving a yield of 1.9%. Again, that’s acceptable but not overly exciting.

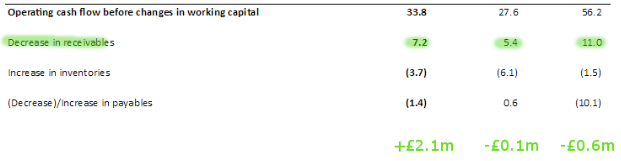

The price/free cash flow ratio of 12.5 implies that free cash flow has exceeded earnings over the last year. However, this seems to be due to McBride collecting payments from customers more quickly, so I wouldn’t read too much into this. Falling receivables generated extra cash for the firm during H1:

Good news from a management perspective, but I think it’s wise to assume that free cash flow will normalise and move back towards earnings per share at some point.

Good news from a management perspective, but I think it’s wise to assume that free cash flow will normalise and move back towards earnings per share at some point.

One final point worth noting is the group’s debt. Net debt fell from £90.9m to £82.9m during the second half of calendar 2016. That’s well within the group’s covenant of 3x EBITDA and below my screening limit of 5x net profit.

Overall, McBride looks fairly priced but not compelling value. Strong momentum and improving quality will be needed to justify a buy, in my view.

Quality: a mixed picture

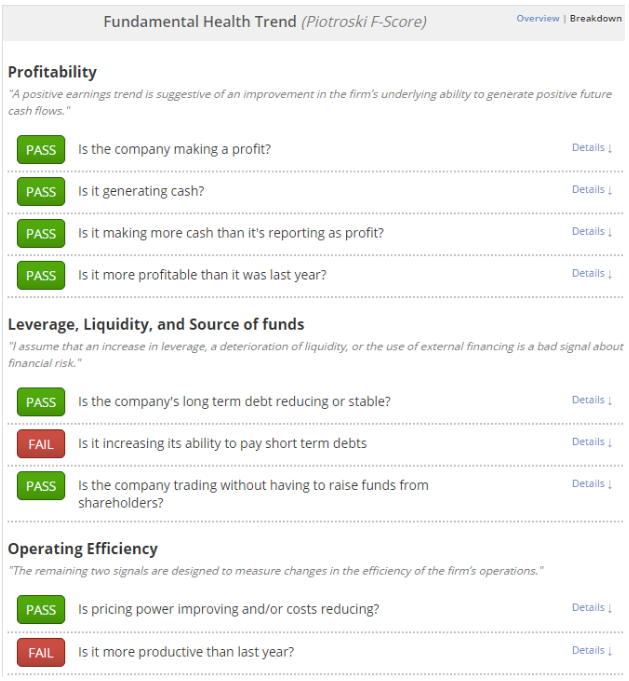

Luckily McBride does step up to the mark in terms of quality. The group’s QualityRank of 85 reflects its high Piotroski F-Score of 7. Looking below the surface here shows rising profits, improved cash generation and growing margins:

Possible risks: I’ve already commented on the group’s improving profitability — ROCE rose sharply last year. But there are two negative points worth mentioning.

The first is that in constant currency terms, revenue fell by 1.9% in 2016 and by 7% during H1. Falling sales with rising profits suggest to me that McBride is still working through the Repair, Prepare stages of its transformation plan. I’d hope to see evidence of top-line growth — the final stage of the plan — at some point in the next twelve months.

The second concern is that the weaker pound may be flattering these figures. Statutory pre-tax profit rose by 44.6% to £18.8m during the first half. But at constant exchange rates, this increase was just 15.3%. Thus the company’s return on capital employed, which uses statutory figures, is being boosted by the weaker pound.

It’s difficult to know how to look at this. There’s no way of knowing when — or if — the pound will regain the ground it lost against the dollar last year.

As a general rule, I usually assume that currency effects will even out over time. I’m prepared to take this view here as I believe McBride’s underlying profitability is improving, albeit at a slower rate than the figures might suggest.

The only question that remains is whether now is the right time to buy. McBride’s share price has doubled over the last two years. Is momentum still strong?

What’s happened to momentum?

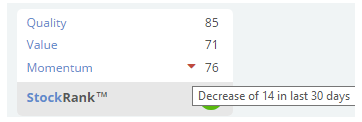

McBride’s MomentumRank has fallen by 14 points to 76 over the 30 days. That’s not a promising start, but it’s worth trying to understand why this has happened.

In this case, the cause of this sharp drop in MomentumRank isn’t immediately obvious. The factors behind the MomentumRank don’t flag up any major weaknesses:

One minor factor is that whereas consensus forecasts were upgraded in March following February’s results, they’ve remained flat in April. This doesn’t concern me, but it is a factor in the MomentumRank calculation (circled).

Another negative factor is McBride’s six-month relative strength (RS 6m), which is now negative. What this indicates is that the stock has underperformed the index over the last six months. The FTSE SmallCap index has gained 9% since October, while McBride stock is unchanged over the same period.

Technical factors such as these can affect a stock’s MomentumRank. But for most investors, I don’t think they’re a reason to stay away from an otherwise attractive stock.

McBride’s adjusted earnings are expected to rise by 40% during the year ending 30 June, and by a further 15% next year. This puts the stock on a forecast P/E of 14.5, falling to 12.6 in 2017/18. Dividend returns are also expected to improve, with a prospective yield of 2.2% on the cards for the current year.

These figures look attractive to me. Assuming the group continues to make progress with its transformation plan, we should see a move into top-line growth over the next year.

I’m buying

I’m going to add McBride to both the SIF portfolio and my personal portfolio on Wednesday this week. This is part of a shift in my own investing that I’ll cover in more detail later this month.

Roland owns shares of McBride, Unilever and J Sainsbury.

Source: http://www.stockopedia.com/content/sif-portfolio-can-i-clean-up-with-mcbride-179110/