Commercial & Residential Real-Estate Bubble Once Again a Risk to “Financial Stability,” and Fed’s Rosengren is Worried

by Wolf Richter, Wolf Street:

![]() The Fed caused it, but it won’t do much to contain it.

The Fed caused it, but it won’t do much to contain it.

Last year, Boston Fed President Eric Rosengren — considered a “dove” on the Fed’s policy-setting committee — started warning about the commercial real-estate bubble in the US and what its demise could do to banks. But in his speech on Financial Stability on March 22 in Indonesia, he added what I’ve come to call “Housing Bubble 2” to his ever more emphatic concerns.

Like all central bankers, he can’t warn publicly about an approaching problem because it could trigger the very problem he’d be warning about. In this manner, no one at the Fed saw the last bust coming. So Rosengren started out his presentation, “Financial Stability: The Role of Real Estate Values” – by clarifying this: “First, I am not here today to predict problems, but rather to suggest we continue working to head them off.

The phrase, “continue working to head them off,” is ironic because he also pointed out what has caused these problems: “very low interest rates” that were “wholly necessary” and that he “strongly supported.”

But the risks are massive.

Rosengren finds that “the root cause of the financial crisis was a significant decline in collateral values of residential and commercial real estate” and “exposures across the banking system that are correlated and sizeable.”

Real estate becomes a trigger for a financial crisis because of its high leverage. For banks, these properties are collateral. When property values tank, the collateral is impaired. Defaults rise. Then broader problems spread into the economy. Property owners experience a reduction in income. Homeowners see their paper wealth evaporate and financial stress rises. At some point, banks begin to fail.

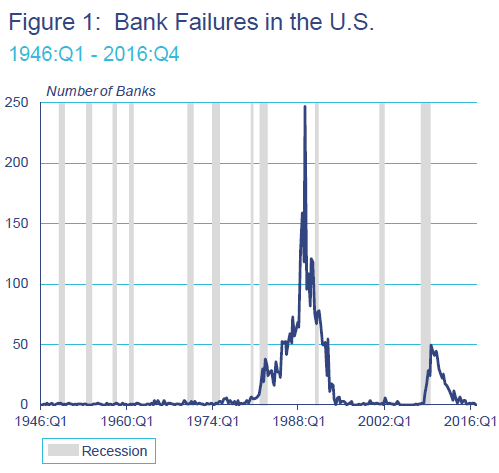

This chart shows the number of bank failures, regardless of size. In the decade before the Financial Crisis, the banks had become huge. Thus, fewer but huge banks failed:

The data includes failures and assistance transactions of commercial banks, savings banks, and savings and loan associations. S&Ls are included beginning in 1980 (source: FDIC, NBER, Haver Analytics).

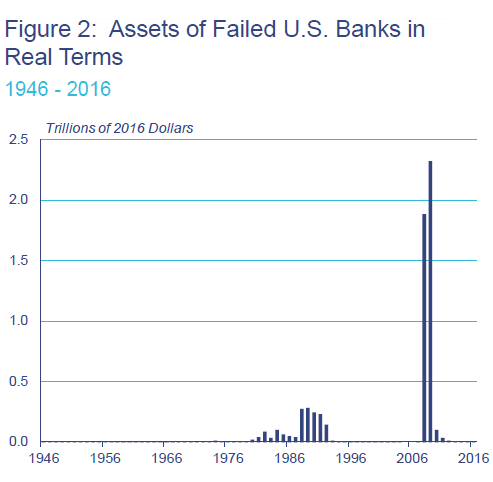

But when these fewer huge banks failed, all heck broke loose. This chart shows the asset values of the failed banks, adjusted for inflation:

As property prices plunged during the Financial Crisis, the balance of CRE loans that were 90+ days delinquent soared to over 7% of outstanding balances; and delinquent home mortgages soared to over 8% of outstanding balances.

Real estate has a significant financial stability implication because real estate tends to be leveraged by the owners, and those loans represent a significant exposure for financial institutions that are themselves highly leveraged.

As losses from these assets (the loans) hit banks’ capital, the banks shrink their lending, which crushes economic activity and also makes it harder to sell properties as potential buyers cannot find banks willing to lend even at depressed prices. Liquidity in the property market dries up.