| Story Views | |

| Now: | |

| Last Hour: | |

| Last 24 Hours: | |

| Total: | |

How to avoid high StockRank underperformers

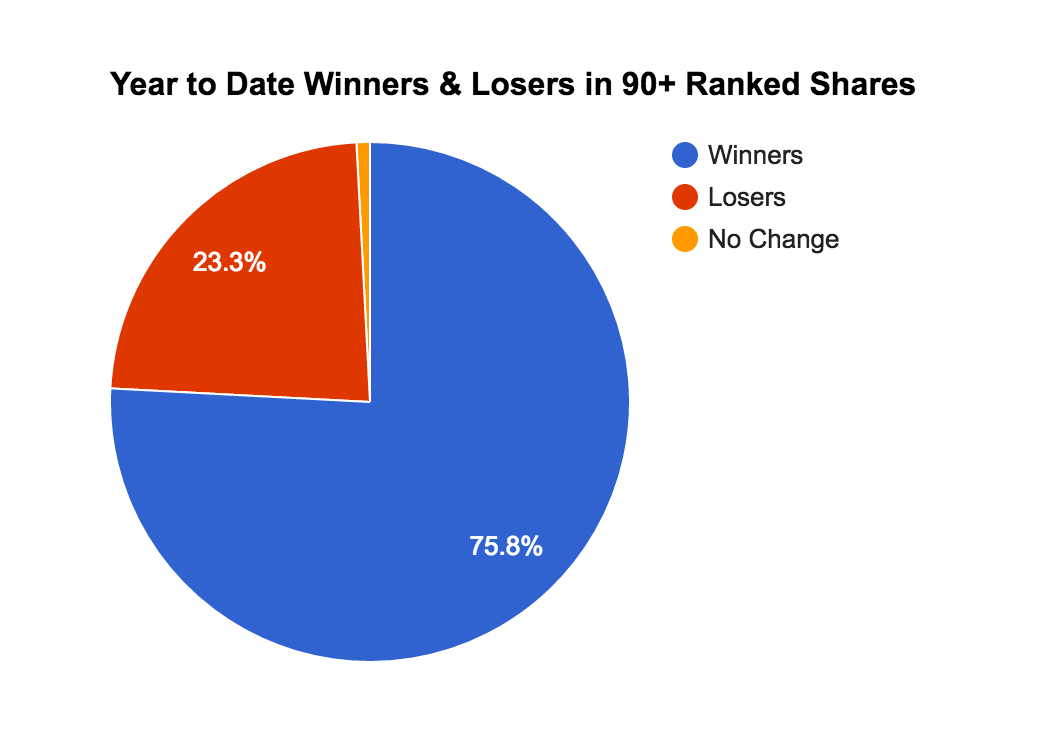

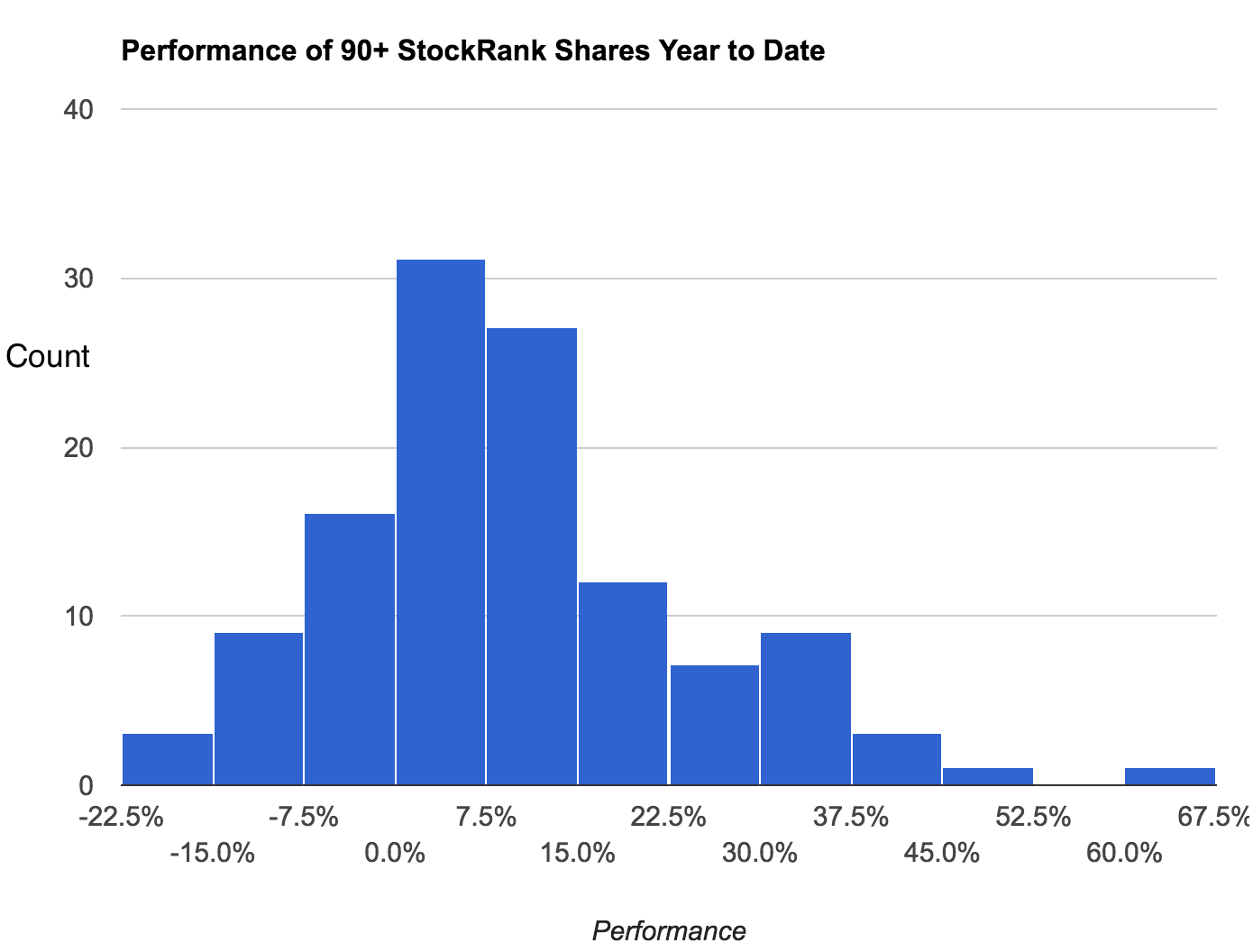

It’s been a cracking start to the year for stock markets, and an even stronger start to the year for high StockRank shares. While the benchmark FTSE All Share Index is now up 4.2% since the end of 2016, the top 10% of UK stocks as ranked by the Stockopedia StockRanks has more than doubled this performance, generating a 10.0% return.

The participation in this rally has been broad. In our performance tracking we focus on investable shares above a £10m market cap. Excluding the microcaps, there were 120 UK stocks ranked 90 or above at the end of 2016. Of these, 91 have been winners (with higher share prices today), while 28 have been losers (with lower share prices today).

While these headline figures make great reading, it’s no comfort for those who have bought the losers, and as ever, among the losers are some popular shares.

Picking losers is inevitable in the stock market. Not even Warren Buffett is immune (he bought Tesco at the top after all). So the key to enduring profits is twofold. Minimising the number of losers bought, and minimising the scale of the losses from each.

When things don’t Go-Ahead

An example of a high ranking share that took a hit recently is Go-Ahead Group . Go-Ahead Group is a very well known company in the UK. It’s been a member of the FTSE 250 index for a long time and operates many London buses and English rail franchises. Perhaps as a result of its status, many subscribers own it.

I purchased some shares in GOG on 17th Feb when the stock rank was 99. They released some poor results and now the stock rank is showing as 65 but I cannot find any discussion or advice on whether to sit tight and ride it out.

Markets can be brutally unforgiving on profit warnings. Here’s a chart of Go Ahead Group’s price collapse on its profit warning announcement and afterwards. (with annotations drawn using Stockopedia’s great new Technical Charts ).

Last summer we conducted a study of 245 profit warnings in an eBook titled the Profit Warning Survival Guide. If you haven’t already read it, I highly recommend it. We built a model of what happens before, during and after the archetypal profit warning. The price action of Go-Ahead group has almost precisely followed the script. Go Ahead Group isn’t the first high ranking stock to take a tumble and I can guarantee it won’t be the last.

How to minimise the number of losers bought?

The first step to minimise the number of losers bought is simply to minimise the number of low probability bets taken. The StockRanks are a great first guide here as low ranking shares are almost everything one should want to avoid in a stock – expensive (low value), unprofitable (low quality), underperformers (low momentum). In practically every market in the world we cover, the average low ranking share has underperformed… but taking this as a no-brainer there’s a couple of things we can do to improve the odds further…

1) Watch your biases…

The reality is that most of us reading (and writing) this piece are not full time investors. 95% of us are DIY investors, likely managing our investments in solitary, in our spare time and reaching out online to find some insights to help guide our decisions. Most of us don’t have time to become forensic investors, so we use heuristics (rules of thumb) to make snap decisions. These mental shortcuts make us prone to a whole host of biases when it comes to stock selection.

Some of the most expensive biases include:

- Favouring well known or famous businesses (Familiarity Bias)

- Favouring new or exciting businesses (Lottery bias)

- Favouring stocks that others are buying (Herding Bias)

- Favouring companies run by charismatic CEOs (Halo bias)

- Favouring companies owned by expert investors (Authority bias)

It’s not to say you should deliberately avoid shares that have these attributes. In fact there are some shares I can think of that have all these qualities that have absolutely killed it (e.g. Facebook). But if one’s investment process always favoured the above attributes the portfolio would most likely underperform. The reason is that these attributes are obvious to almost all investors which makes them more prone to be fully priced, and therefore more subject to disappointment.

Countering these biases is not easy but being aware of them is the first step. Here’s a quick thought experiment which may prove my point…

- Open this link in a new tab to review the highest StockRank shares.

- Scan the list quickly for shares to research further.

- Watch your how your mind’s eye is attracted to either familiar companies, or companies with interesting names.

- Watch how your mind’s eye has completely skipped the rest.

As John Templeton has said “if you want to have a better performance than the crowd, you must do things differently from the crowd”. It’s better to act counter to your instincts and start your research with the stocks that you (and others) aren’t noticing. If you find a high ranking share that’s not well known, with an odd name, in a dull business segment, run by reclusive management that nobody seems to be talking about… it may well be the perfect Hidden Champion and hit you a home run.

2) Use a Checklist

It’s a gross simplification, but I believe we fall into two broad camps as investors. We’re either stock pickers or we’re systematic investors. In a previous poll, about 80% of Stockopedia subscribers defined themselves as stock pickers (selecting shares one by one), while 20% defined themselves as systematic (selecting entire portfolios of shares at once).

Neither process is necessarily better, but being a stock picker makes you more susceptible to the biases previously discussed. Stock pickers will also tend to have a much wider variability of outcome. The best can make huge profits, while the worst go bust. Systematic investors are far less likely to have extremes of outcome.

But I think there’s a third segment of investor that may represent the holy grail. Stock pickers who partially systematise their process. Great investors like Charlie Munger (Warren Buffett’s billionaire business partner) and Mohnish Pabrai (successful businessman, investor and author) have waxed lyrically about how their investing has been improved through the use of the humble checklist. Here’s a quote from Pabrai:

Since I put the checklist in place, in 2008 till today, we have made I think more than 30 different investments in the last five years or so. We only have so far, we invested about $200 million. We’ve already exited a bunch of positions and we’ve exited with about $500 million on those positions, and we only lost money on two investments. And the total amount of money we lost from those two investments is less than 5 or 6 million dollars. And I think a large part of that is the checklist significantly brought down the error rate.

I’m not going to tell you how to create your own checklist… as we each have our own experiences, our own strategies and our own mistakes to learn from. But it’s imperative that you create one – online or on paper or in a tool like the checklists tool here. You might think you’ve got a system in your mind, but if it’s not written down how do you know if you are carrying it through? Surgeons amp; Pilots carry out safety checklists during every operation or flight to ensure catastrophic risk is reduced… so why not investors?

To get you started, there are some key red flags worth watching for even in very high ranking stocks. It’s worth checking for debt issues that can flag bankruptcy risks, higher earnings manipulation risks or deteriorating fundamental health. I like to use the ‘professor’s section’ on StockReports as a quick extra sanity check on shares.

Meanwhile high pension deficit issues, poor price momentum or volatile operating histories can be useful checks to add. Qualitative checks on the credibility of management, or heuristics like avoiding companies listed locally but incorporated on the other side of the universe can help avoid the worst frauds (Globo). Maybe the community has some ideas and can add some comments below.

How to minimise the scale of losses from losers?

Even if you put all of the above in place, seeking higher probability investments, managing the monkey mind and using checklists for your research… you will still pick losers. Ultimately there are things we can control and there are things we can’t control. We can’t stop a share from suddenly falling, but we can control whether we continue to own it all the way down. Stopping a loss from turning into a catastrophe is completely within our control.

One of the best books on this subject is The Art of Execution by Lee Freeman-Shor. The author has run a fund of funds for many years and noticed that the money managers that were most successful displayed certain key habits in handling their loser stocks. He categorised them as either:

- Assassins – when shares declined, this investor archetype ruthlessly cut their losers. i.e. they used stop losses normally around the 20% level.

- Hunters – when shares declined, this investor archetype bought more. Lowering their average purchase prices so that they’d make far higher profits on the rebound.

If you are an assassin you’ll have higher trading costs, if you are a hunter you will averaging down on losers (which you don’t want to do if they don’t bounce back!). But he found that these two behavioural patterns led to most success.

The worst investors, on the other hand, always displayed the same trait. They were…

- Rabbits – when share prices decline, like the proverbial Rabbit in the headlights, these investors freeze. By doing absolutely nothing, they leave themselves exposed to losing everything.

My experience with individual investors is that the majority are rabbits. Don’t be a rabbit. There are also many who attempt to be Hunters (in Freeman-Shor’s taxonomy) but only compound their original mistake… by buying more of a stock that only proves to get worse. I have thought for a long time that individual investors should almost always have a default Assassin mode… cut losses unless there is a huge reason not to. From a ranking perspective I would only consider doubling down on very high QualityRank stocks.

How and when should you cut losses? My own rule of thumbs are as follows:

- Share price declines 20%… I cut.

- Big StockRank declines… I cut.

- Profit Warnings or bad earnings misses… I cut.

- Significant negative developments… I cut.

Often these traits all come together at once, which makes it a heck of a lot simpler to act.

Don’t rationalise that you shouldn’t sell for some made up reason (‘I won’t sell as it crystallises capital gains tax’, ‘I can’t sell as the spread is wide’, ‘I can’t sell as I don’t know what else I’d buy’, ‘I can’t sell as my long lost grandmother bought this share for me and I’d feel guilty’)… start treating selling as a form of insurance. We don’t enjoy paying our insurance on our homes, travel or health… but we feel much more certain that if catastrophe happens we’re well prepared. So start considering taking a loss as a form of insurance. Start accepting them as a cost of business. Let losses become your friend in the market.

Now let your winners run…

Minimising buying errors is of course part of the process, but of far more importance is managing your losers. Maybe I shouldn’t be focusing so much on the downside in a bull market. But I’ve always run by the principle that you should minimise the downside you can leave the upside to the gods. Meanwhile if you do have winners… don’t snatch at them by taking profits… let them run. I’ll leave you with this nugget from Jesse Livermore:

Traders who can both be right and sit tight are uncommon. I found it one of the hardest things to learn. But it is only after a stock operator has firmly grasped this that he can make the big money.

Source: http://www.stockopedia.com/content/how-to-avoid-high-stockrank-underperformers-177047/